Good Earnings Are Getting Crushed But Here Is How You Can Profit

The new 2026 rule: Punish complexity, reward simplicity.

Earnings season is back baby!,

And if the opening week is any indication, we are settling in for a quarter that is going to be incredibly specific about what it rewards and ruthless about what it punishes.

To understand why the tension is so high, you have to look at the context of where we are standing right now.

It is early 2026, stock prices have rallied near all time highs, and investors have essentially pushed all their chips into the center of the table betting on a perfect economic landing.

This is not just a routine check up on corporate profits, it’s high pressure test to see if these companies actually deserve the massive price tags the market has slapped on them.

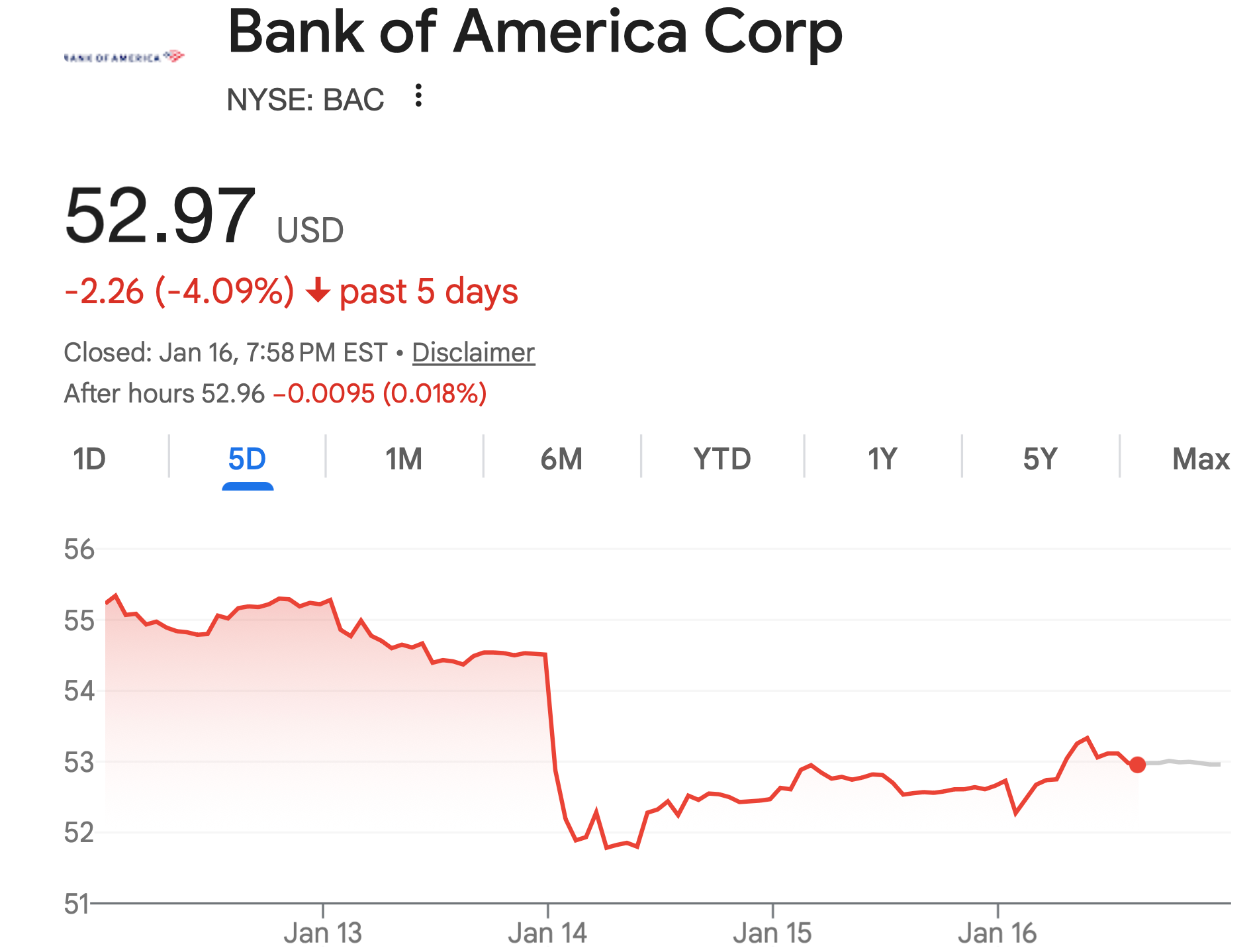

We saw this dynamic play out immediately with the banks last week which gave us a perfect tale of two markets.

On one side, you had massive institutions like JPMorgan (down nearly 3%) for the week.

Bank of America (down 4%) delivering results that were numerically fine, essentially solid report cards that met all the technical requirements.

However, investors hammered their stocks because those earnings came wrapped in layers of regulatory headaches, potential capital requirement increases, and general political noise.

The market simply does not want to deal with complexity right now.

On the other hand, pure investment banks like Morgan Stanley were the life of the party because their story was incredibly simple to understand.

They showed that deal making is back, fees are flowing, and there isn’t a massive government cloud hanging over their future profits.

This set the tone for the entire quarter, signaling that investors are willing to pay a premium for simplicity and clean execution.

But if your results come with administrative drama or legal baggage, you are going to the penalty box regardless of how much money you actually made.

This extreme pickiness makes perfect sense when you step back and look at the valuation of the stock market today.

The S&P 500 is trading at price levels that we haven’t seen since the post-COVID euphoria or even the dot-com bubble, which means the index is being priced like a high-growth startup rather than a stable basket of companies.

When you pay a price that implies perfection, you naturally expect a perfect outcome.

This creates a dangerous setup for companies this quarter.

Wall Street has set the bar relatively low for the last three months of earnings, expecting only about 7% growth, which most companies will likely step over easily.

But here is the catch.

The market has already looked past this quarter and is pricing in a massive year for 2026, betting on double-digit earnings growth and significantly fatter profit margins.

That means simply beating the estimate for the recent quarter is just the bare minimum requirement to keep a stock from crashing.

It is no longer enough to just pass the test, companies have to promise they are going to ace the entire year ahead.

If a management team hints that the future looks even slightly murky, the trap door opens, and there is zero financial cushion for disappointment because all the optimism is already fully baked into the price.

The central character in this high-stakes drama still remains AI but the plot has shifted dramatically from where we were six months ago.

We have officially moved past the phase where a CEO could simply mention their exciting AI pilot programs and watch their stock price pop.

That grace period is over.

Wall Street is done hearing about experiments and want to know exactly how AI is hitting the bank account today.

For software companies, this means showing that AI features are allowing them to charge customers more money or stop them from cancelling subscriptions.

For boring industrial companies, it means proving that AI robots or automated scheduling are allowing them to do significantly more work without hiring any new people.

The investment focus is rotating away from the infrastructure trade of buying the expensive chipmakers and data centers that everyone already owns and moving toward the productivity layer.

The new gold rush isn’t about buying the companies selling the shovels anymore, it is about finding the regular companies that are actually finding gold with those shovels by becoming more efficient.

We also need to clarify the spending side of the AI equation because the headlines are going to get confusing.

You will likely hear a lot of chatter about how the growth rate of AI spending is slowing down, dropping from explosive jumps to more moderate levels.

The bears will try to tell you this means the AI boom is busting, but that is just bad math.

It is simply the law of large numbers at work because you cannot keep doubling your spending every single year when you are already spending tens of billions of dollars.

The absolute mountain of cash being poured into chips, cooling systems, and data centers is still growing, but investors are looking for maturity.

They want to hear management teams explain that this spending is stabilizing into a steady, productive rhythm rather than just a reckless arms race.

The winners this season will be the companies that can explain they are spending billions but getting twice as much efficiency out of their new equipment.

And the losers will be the ones who look like they are burning cash just to keep up appearances.

Why Owning The Winners Is Now Dangerous

Looming over all of these company specific stories is a massive macroeconomic headache involving the tug of war between the US dollar and trade policy.

Recently, the dollar has been getting weaker, which in normal times is great news for American companies because it makes their products cheaper for foreign buyers and boosts international sales figures.

However, the threat of new tariffs is acting as a massive buzzkill that complicates this math.

Tariffs essentially function like a silent tax on corporate profits.

The smart money estimates that a significant hike in tariffs could wipe out a meaningful chunk of the entire market’s earnings power.

This creates a confusing situation where a company might report great revenue numbers thanks to the weak dollar but disappointing profit margins because of tariff fears.

The critical skill for companies right now is pricing power, which is the ability to pass those extra tariff costs on to the customer without driving them away.

If a company cannot raise prices, they are going to get squeezed, and you do not want to be holding their stock when they announce that their profit margins are shrinking.

Finally, navigating this market requires understanding the positioning trap.

Because everyone has piled into the same popular winner stocks, the market has become incredibly lopsided.

This creates a volatility gap where the overall market looks calm, but individual stocks are violently swinging around.

If you own the crowded AI darlings, the risk-reward is terrible because if they report amazing news, the stock might barely move since everyone already expects it.

But if they miss, the exit door is tiny, and everyone tries to leave at once, causing a crash.

On the flip side, the hated stocks that everyone is betting against are like coiled springs.

If a heavily shorted company like Moderna or PayPal reports news that is merely not a disaster, the short sellers panic, buy back the stock to cover their bets, and the price rips higher.

This sets up a very specific playbook for finding opportunities.

Here is exactly how I am positioning for this earnings and how you can profit from all of this.

Keep reading with a 7-day free trial

Subscribe to Investinq to keep reading this post and get 7 days of free access to the full post archives.