The Credit Market Is Collapsing

AI is killing borrowers

In April 1912, the RMS Titanic hit an iceberg at 11:40 PM.

By midnight, just twenty minutes later, the ship’s engineers already knew it was going to sink.

Up on the first-class deck, the band played on as passengers sipped brandy, some even tossing fresh chunks of ice from the deck into their glasses.

And the orchestra didn’t stop until 2:15 AM.

The gap between what the engineers know and what the passengers know is the most dangerous twenty minutes in any crisis.

Right now, the private credit market is somewhere between 11:40 and midnight.

The engineers, Morgan Stanley, UBS, and the IMF are already staring at the hull.

The passengers, $1.8 trillion worth of pension funds, insurers, and everyday investors are still on deck, sipping their brandy, wondering why everyone looks a little tense.

Let me be the person who taps you on the shoulder.

What is private credit, and why should you care?

Private credit is shadow banking.

It’s what happens when your local bank decides a company is too risky to lend to and a giant investment fund steps in instead.

Funds run by names like Apollo, Ares, Blackstone, KKR, and Blue Owl stepped into that gap after 2008, when tighter bank regulations forced lenders to retreat from riskier deals.

And they never looked back.

Today, private credit manages roughly $1.7–1.8 trillion in loans, mostly to mid-sized companies that can’t tap the public markets.

For years, the trade was almost too good to be true.

Investors poured in because the yields were juicy, several percentage points above what boring bonds were paying.

The funds were lent at floating rates, so when interest rates rose, the funds earned even more, and the returns were staggering. Over the 18 months ending January 2025:

• KKR returned 103%

• Blue Owl returned 81%

• Apollo returned 78%

• Ares returned 68%

Sounds incredible, but here’s the catch.

These loans are completely illiquid, no exchange, no market price, whatever the fund manager decides they’re worth.

But the funds sold themselves to retail investors, pension funds, insurers, high-net worth individuals with the promise of semi-regular withdrawal windows.

You could theoretically get your money back monthly or quarterly.

Then everyone decided they wanted their money back at once and that’s when the architecture cracked.

The gates are closing

The crisis of confidence arrived in early 2026, fast and ugly.

Blue Owl Capital was first back in February, it didn’t just pause withdrawals from its retail private credit fund, it shut them down for good.

Mohamed El-Erian, the former PIMCO CEO, a man who has seen a credit crisis or two, immediately drew comparisons to August 2007, when BNP Paribas froze three funds over illiquid asset valuations.

That was the opening shot of the global financial crisis, and then came the dominoes.

Morgan Stanley and BlackRock tightened restrictions.

In March 2026, Ares Management capped quarterly withdrawals at 5% after investors tried to redeem 11.6% of a $10.7 billion fund.

Apollo followed the same day with an identical 5% cap on a $25 billion vehicle, after redemption requests hit 11.2%.

In Q1 2026 alone, $13 billion in total redemption requests and over $4.6 billion still unresolved.

The stock market had thoughts about this.

• Apollo: down more than 23% in 2026

• Ares: dropped over 12% in a single session

• Blue Owl, KKR, Blackstone: all double-digit declines

The message from markets was blunt nobody trusts the price tags on these assets anymore.

Why? Because of two letters: AI

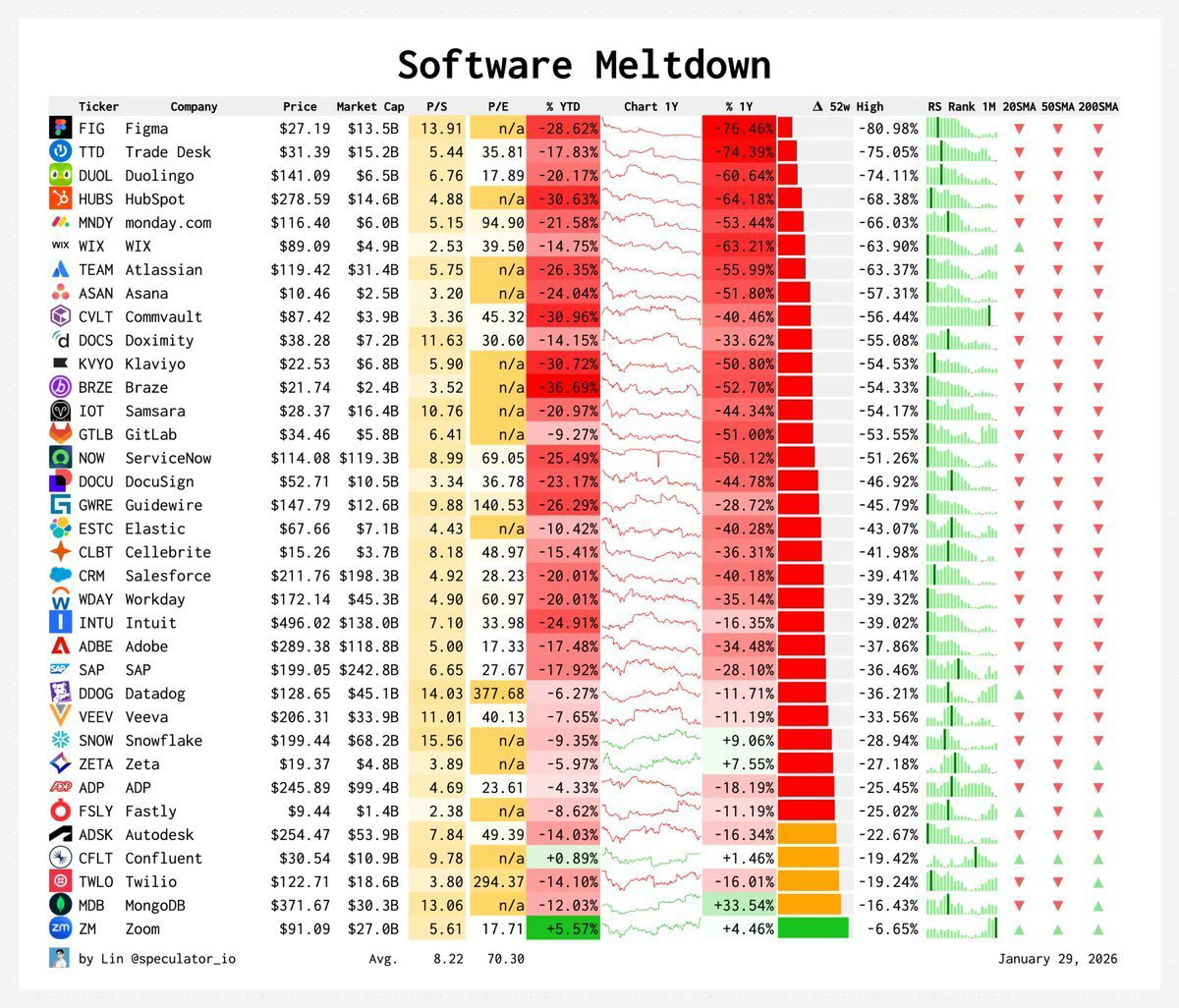

The AI wildcard: why software loans are ground zero

Over the past decade, private credit funds fell in love with software companies.

Specifically SaaS, software businesses with predictable recurring revenue, sticky customers, and no factories to burn down making them seem like the perfect borrowers.

Outstanding loans to SaaS firms grew from roughly $8 billion in 2015 to over $500 billion by end-2025.

That’s roughly 19% of all direct private credit loans about one in every five dollars flowing into software companies.

Then AI ate the software sector’s lunch.

Agentic AI tools started doing the complex, billable professional tasks that many software firms charge for.

The revenue models underpinning hundreds of billions in private credit loans began to look shaky.

Software company stocks fell nearly 30% between October 2025 and February 2026.

And here’s the cruel twist nobody planned for.

Software loans are nearing a maturity wall about 11% come due by 2027, with another 20% hitting in 2028.

Companies that can’t refinance because AI disrupted their business model will default and unlike a manufacturer that has equipment to seize in bankruptcy, a software company’s main asset is its code.

Which is now being written for free by the AI that killed its customers.

Morgan Stanley estimates direct lending defaults could reach 8% approaching COVID-era highs driven largely by AI disrupting software borrowers.