🤯 This AI Bet Could Change Everything

Wall Street is pricing yesterday, this company is building tomorrow.

If you want to understand one of the single biggest opportunity in the stock market right now, you don’t need a degree in finance.

You just need to understand a simple problem of physics that is currently costing the world’s biggest companies trillions of dollars.

For the last twenty years, the internet, the thing that powers your Netflix, your banking app, and your emails was built on a specific type of microchip called a CPU.

Think of a CPU like a really good Office Manager.

It’s organized and it’s reliable.

It can do a thousand different things one after another: “Open this spreadsheet, send this email, load this webpage.”

It is designed to be a multitasking generalist.

Because of this, companies like Amazon, Microsoft, and Google spent two decades building massive data centers that were essentially giant office buildings for these managers.

They were quiet, air-conditioned rooms where rows of servers hummed along, sipping a polite amount of electricity.

Everything was efficient and fine.

Then, the aliens landed.

In late 2022, ChatGPT arrived, and the world realized that AI doesn’t work like an Office Manager.

AI doesn’t need to multitask, it needs to do math.

That’s because every thought an AI has is really just numbers being multiplied and added together.

AI models turn words, images, and sounds into huge grids of numbers called matrices.

To figure out the next word in a sentence or identify a cat in a photo, the model runs the same math operation on those numbers over and over, multiply, add, repeat millions or billions of times.

So instead of doing lots of different tasks one after another, AI is doing one kind of task millions of times at once.

That’s why the old CPU based world broke and why GPUs, built for massive parallel math, took over.

GPU’s are made by a tiny company you might have heard of called NVIDIA.

If the CPU is an Office Manager, the GPU is a team of 10,000 mathematicians screaming answers at each other in a room.

But here is the trillion dollar problem: You cannot put these new alien brains into the old office buildings.

It is a physical engineering nightmare.

A rack of old CPU servers generates about as much heat as a few hair dryers.

A rack of modern AI chips generates as much heat as a blast furnace.

If you plug a modern AI supercomputer into an old Amazon or Google data center, you will quite literally melt the power cables and set the room on fire in minutes.

The old air conditioning systems, which just blow cold air through vents, simply cannot move the heat away fast enough.

This means the world’s biggest tech companies are sitting on empires of legacy infrastructure that is suddenly obsolete for the new hot thing.

They are scrambling to retrofit, but it is slow, expensive, and painful.

This disaster created a massive opening for a new breed of company: the “Neocloud.”

These are companies that started from scratch with zero baggage.

They buy empty land and build AI Factories designed specifically for these hot, hungry GPUs.

They use liquid cooling (piping fluid directly to the chips) and specialized networking cables that cost more than a Ferrari.

They don’t sell web hosting or email or photo storage.

They sell raw, unadulterated intelligence.

And that brings us to the most fascinating, and perhaps most misunderstood, player in this arena.

Drum roll please and say hello to my little friend newest position.

Nebius Group (NBIS). Side Note: You can track every thesis and previous position in this live spreadsheet so you can see the exact price we entered at in real time.

The “Born Rich” Advantage

Usually, when you hear about a hot new AI stock, it’s some startup run by three guys in a garage who were mining Bitcoin six months ago.

They have a cool PowerPoint, but they have to beg venture capitalists for money to buy even a handful of chips.

Nebius is weird.

It is technically a new company, but it’s actually a 22 year old tech giant that faked its own death and was reborn in Amsterdam.

Until 2022, there was a company called Yandex.

People called it “The Google of Russia.”

It was a NASDAQ-listed behemoth with world class search engines, self driving cars, and thousands of the best engineers in Europe.

But when the geopolitical situation exploded, the leadership did something radical.

They decided to amputate the company to save it.

They executed a clean break. They sold all the Russian assets, the search engine, the taxi apps, the consumer brands for over $5 billion.

They left the country completely.

What remained was a Dutch holding company, renamed Nebius, which kept the only things that mattered for the future:

The patents.

The software code.

The 1,300 top engineers who fled to the West.

A massive war chest of billions of dollars in cash.

So when you look at Nebius, you aren’t looking at a scrappy startup.

You are looking at a veteran technology army that was “born rich.”

The Deep Dive: How Do They “Own the Stack”?

This is the most important part of the thesis.

Most AI Clouds are actually just assemblers.

They buy Dell servers, rent space in an Equinix data center, and install standard software.

They are middlemen.

Nebius is vertically integrated.

That’s fancy MBA speak for: “We cook our own food, grow our own vegetables, and built the kitchen ourselves.”

Here is exactly how they own the stack, from the dirt to the code:

Layer 1: The Metal (The Hardware)

Nebius doesn’t just buy off the shelf server racks.

Because they have those 1,300 ex-Yandex engineers, they design their own proprietary server racks and power distribution units.

Why does this matter? Heat.

Their flagship data center in Finland is a masterpiece.

It captures the massive heat generated by the AI chips and pipes it into the local town’s district heating system, warming homes in the winter.

The Result: A “Power Usage Effectiveness” (PUE) score of 1.13.

The Benefit: The industry average is much higher. A lower score means a lower electricity bill. A lower electricity bill means higher profit margins.

While competitors are paying to vent heat into the atmosphere, Nebius is recycling it.

Layer 2: The Orchestration (The “Soperator”)

This is the secret weapon for the nerds.

In the world of supercomputers researchers speak a language called Slurm.

It’s old-school, rigid, but incredibly fast.

In the world of modern apps (startups), developers speak Kubernetes.

It’s flexible and runs on the cloud.

Usually, you have to pick one.

It’s like choosing between a manual transmission racecar (fast but hard to drive) and a Tesla (easy but automated).

Nebius built a proprietary tool called “Soperator” (Slurm Operator).

It translates between the two languages.

It allows top-tier AI researchers to run their old-school, high-performance science experiments inside the modern, flexible cloud environment.

This makes their platform incredibly sticky. Once an AI lab builds their workflow on Soperator, it is very painful to leave.

Layer 3: The Platform (MaaS)

Finally, they offer Managed Services.

Instead of just giving you a raw GPU and saying good luck, they provide the software environment pre-configured.

If you want to train a model using PyTorch, Nebius has a click-to-deploy environment ready.

This attracts the mid-market companies who need AI but don’t have 50 PhDs on staff to configure servers.

Because Nebius owns the hardware design, the software, and the data center operations, they capture the margin at every step.

CoreWeave Model: Rent equipment -> Pay Interest -> Pay Landlord -> Small Profit.

Nebius Model: Buy equipment cash -> Own Building -> Keep All Profit. Analysts believe this will eventually lead to 60-70% gross margins, compared to the razor-thin margins of renters.

The $17.4 Billion Hammer Drop

For most of 2024, this was all just a nice story. Investors were skeptical. “Sure, you have cool tech,” they said, “but who is actually going to buy from you?”

Then, in late 2025, Nebius dropped the hammer.

Microsoft signed a definitive agreement to rent Nebius’s GPUs.

And this wasn’t a small trial, it was a deal worth $17.4 billion committed over 5 years.

Microsoft, the third most valuable company on earth, effectively admitted it couldn’t build infrastructure fast enough and needed Nebius’s help.

This deal involves Nebius building a massive new data center in New Jersey specifically to serve Microsoft’s needs.

Shortly after that, Meta (formerly known as Facebook) followed up with a $3 billion deal.

These contracts changed everything.

They effectively guaranteed Nebius’s revenue for the next half-decade.

They also solved the financing problem.

Because Nebius has a signed contract from a Triple-A credit-rated company like Microsoft, banks are now lining up to lend them money to build the data centers.

This created a virtuous cycle:

The contracts proved the tech works.

The contracts secured the cheap debt financing.

The funding builds the capacity to sign more contracts.

The Scorecard: Numbers Go Up 📈

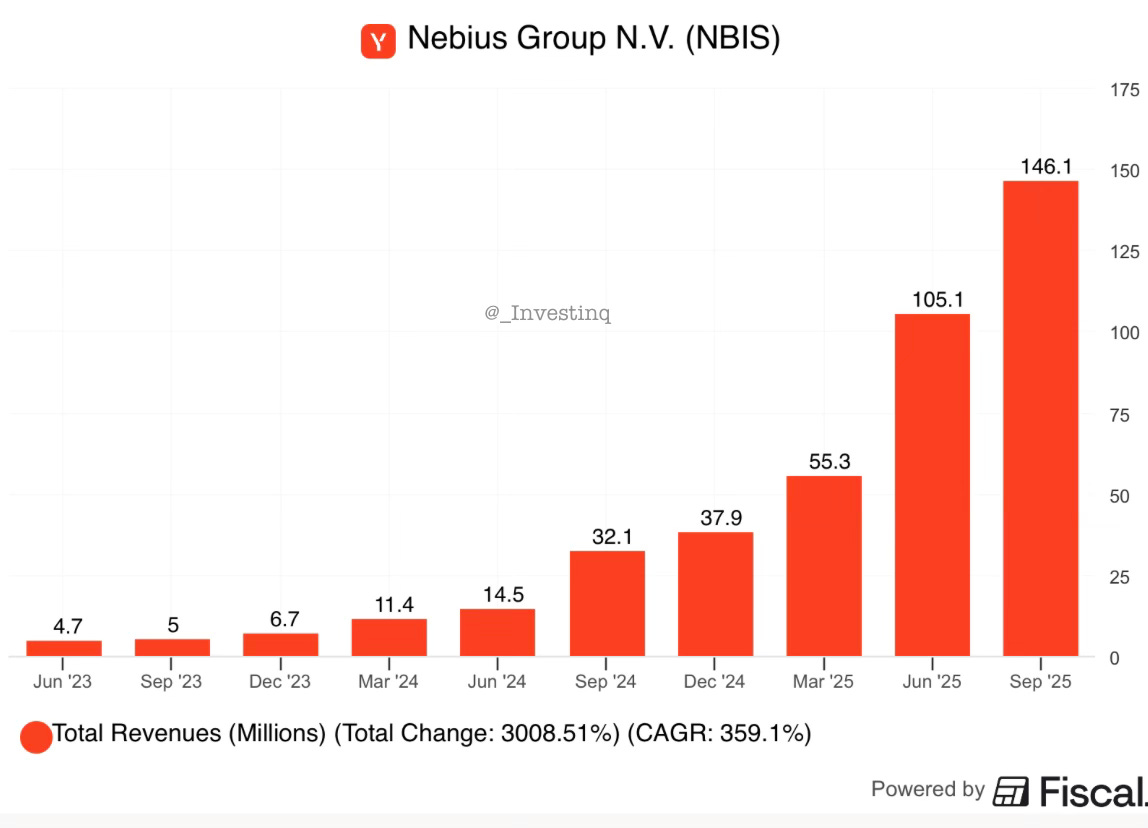

Let’s look at the scorecard, because the numbers are getting wild.

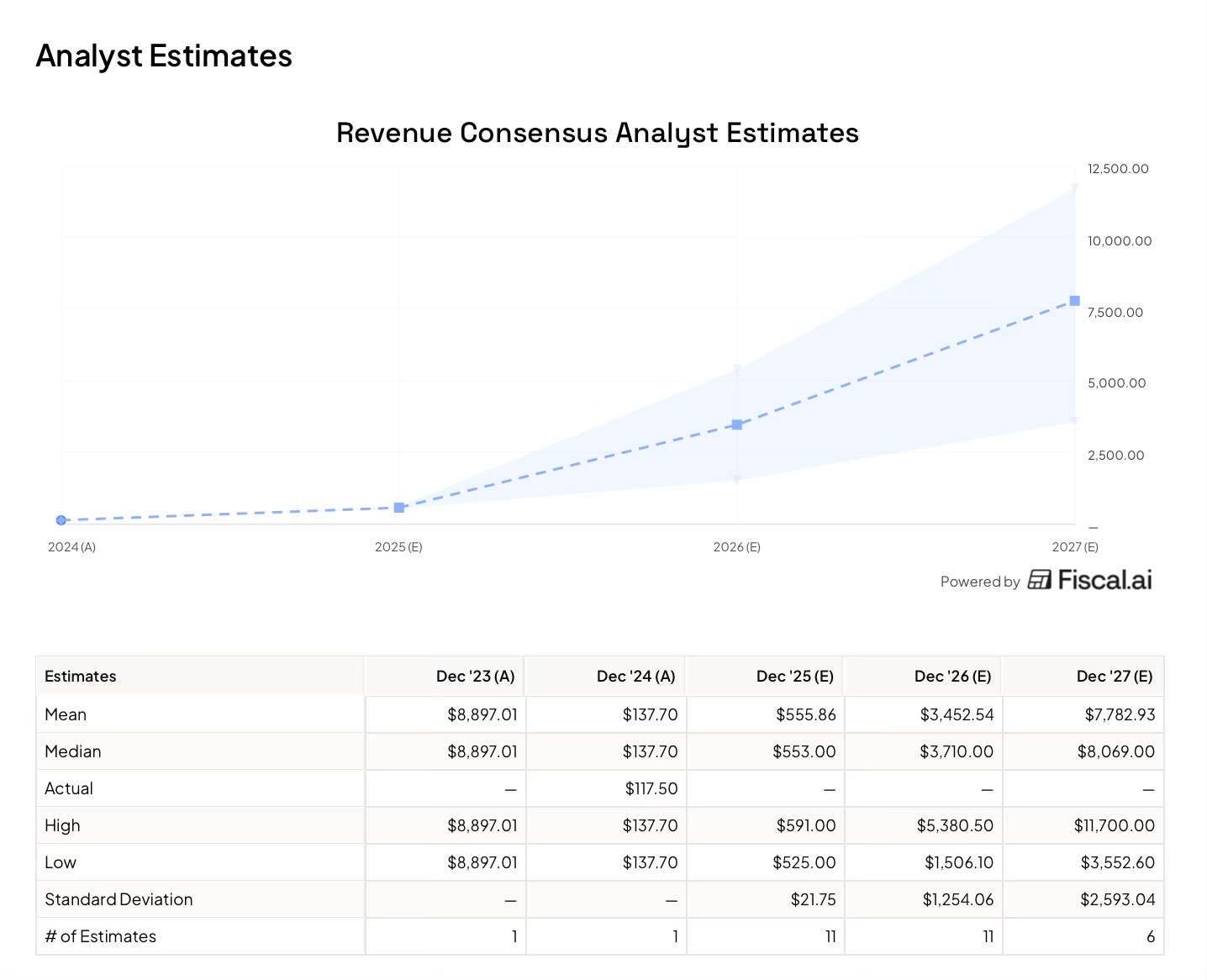

In the third quarter of 2025, Nebius revenue grew 355% year-over-year to $146 million.

Side Note: These charts were made with Fiscal.AI, which I use daily for structured financial data and analysis. Use this link to get 15% off all plans.

They are forecasting to hit an annualized revenue run rate of $1 billion by the end of 2025.

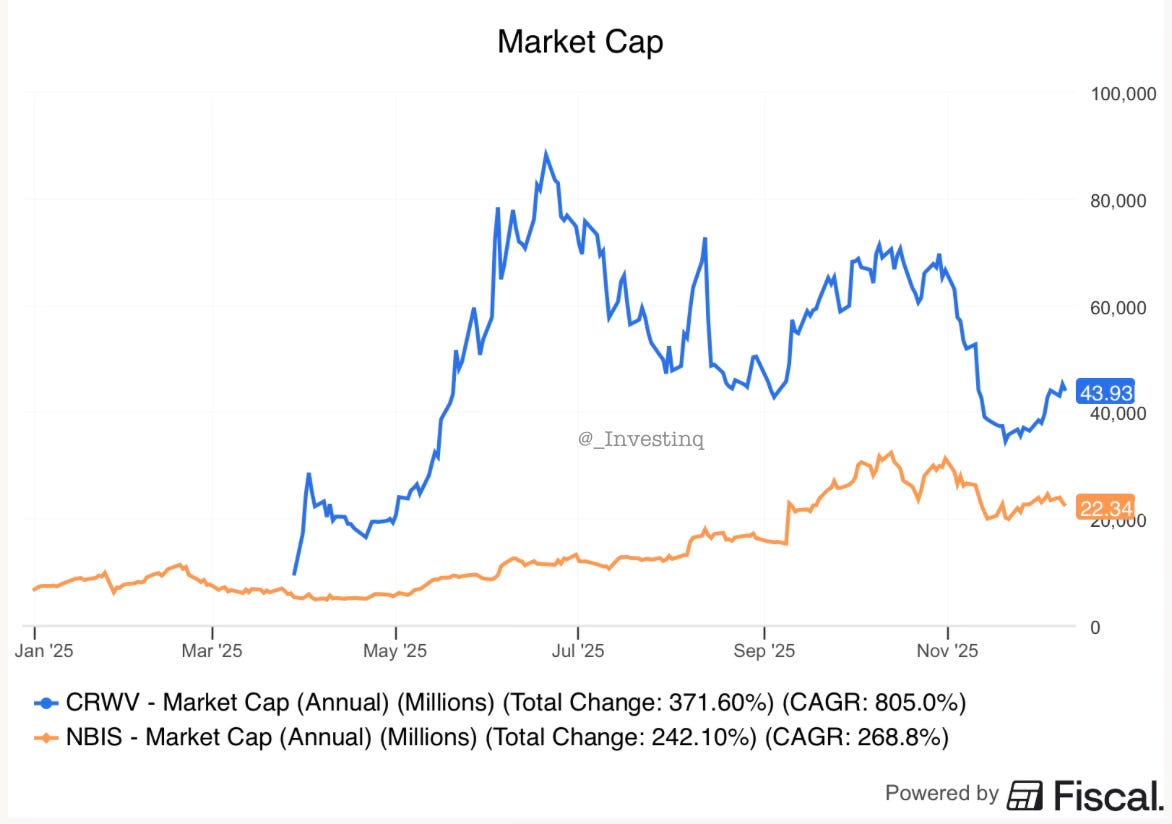

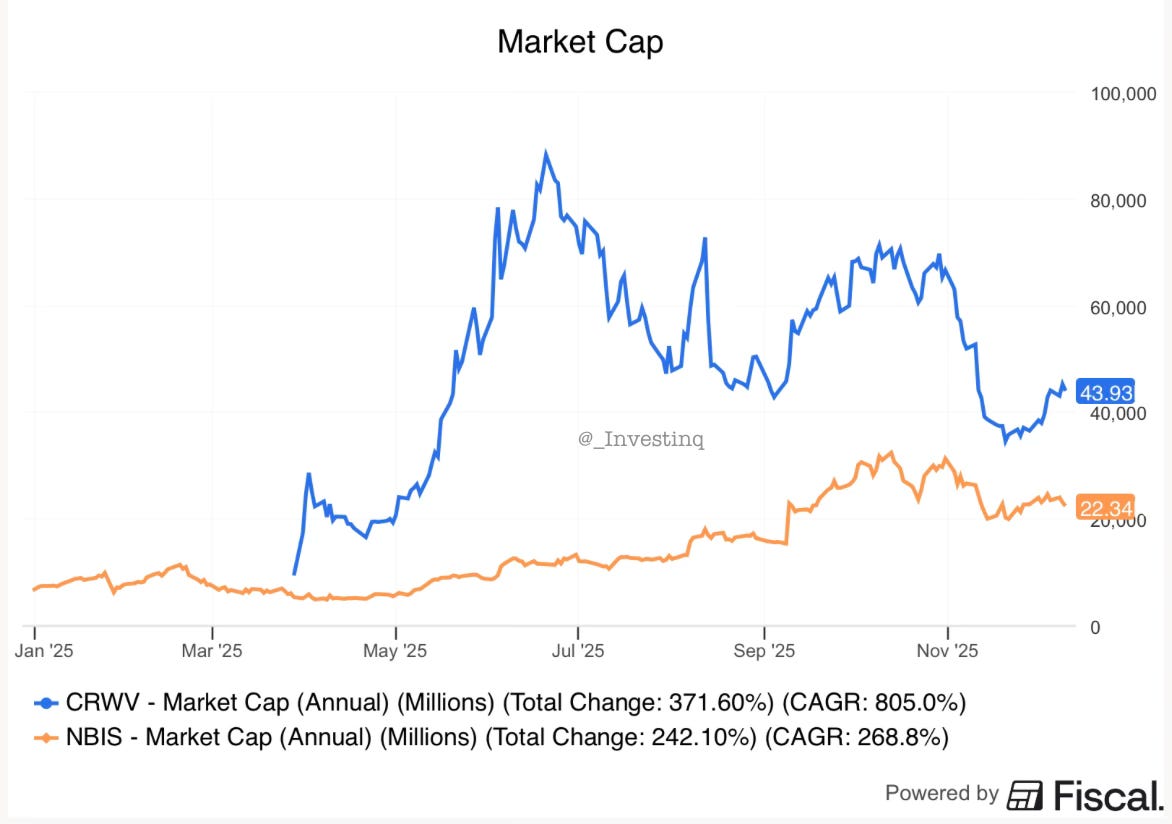

Nebius’s main rival is a company called CoreWeave.

CoreWeave Valuation: ~$44 Billion.

Nebius Valuation: ~$23 Billion.

But the gap becomes even more extreme when you compare forward fundamentals versus trailing ones.

Right now, on trailing revenue, Nebius screens as expensive.

The company only posted $363M in revenue over the last twelve months, which makes multiples like EV/Sales of 66x and EV/EBITDA of -96x look eye watering on paper.

(Quick translation: EV/Sales shows how much investors are paying per dollar of revenue. EV/EBITDA shows how much they’re paying relative to profits. A high EV/Sales or a negative EV/EBITDA just means the company is still in heavy build-out mode and hasn’t scaled profitability yet.)

Nebius is guiding to $750M to $1B in annualized revenue by year end 2025.

And the analyst estimates reinforce that trajectory, consensus revenue jumps to ~$556M in 2025, ~$3.45B in 2026, and ~$7.78B in 2027, with even the low end estimates landing well above today’s trailing revenue base.

When you reprice Nebius on that forward revenue base, the entire valuation profile collapses downward:

At a $1B run-rate, Nebius trades at roughly 24x EV/Sales,

While CoreWeave trades closer to 40–55x forward sales.

Suddenly Nebius isn’t expensive at all.

And the deeper you go, the wider the gap becomes.

Nebius owns its infrastructure outright, a massive advantage as scale increases and depreciation begins to flatten operating costs.

CoreWeave, in contrast, leans heavily on debt financing and leased equipment, which ties its long-term margins to interest rates, refinancing cycles, and hardware renewal schedules.

Nebius is also aggressively expanding its global footprint, bringing new data center capacity online across the U.S., Europe, and the Middle East, with 100MW+ of deployments planned for 2025.

This is the same pattern of infrastructure ramp that fueled CoreWeave’s valuation explosion.

Then there’s the Nvidia angle.

Nebius secured a strategic partnership with Nvidia and is among the first cloud providers to offer Blackwell Ultra instances, a signal that Nvidia doesn’t see Nebius as a second-tier operator but as a front-line infrastructure partner.

Combine that with long-term contracts, ARR acceleration, global expansion, and a differentiated software stack (Slurm-based orchestration, automatic recovery, proactive system health checks), and you get a business the market is still valuing based on yesterday’s version even though the 2026–2027 version is what should be priced in.

In other words: The market is using a rear-view mirror to price a rocket that’s already pointing straight up.

The Hidden Bonus Level: Sum of the Parts

Finally, there is one last piece of the puzzle that makes this stock a value play in disguise. It’s called the Sum of the Parts.

When you buy Nebius stock, you aren’t just buying the cloud business.

You are getting three other businesses for free that are hidden inside the company structure.

Avride: The former self-driving car division of Yandex. In October 2025, Uber invested $375 million into Avride, valuing it at several billion dollars. Nebius owns over 80% of this company. It acts as a massive safety net; even if the cloud business struggles, Nebius could sell Avride to a company like Uber or Tesla and return a huge amount of cash to shareholders.

Toloka: A platform for labeling data to train AI. Jeff Bezos’s VC fund invested in it recently.

TripleTen: An education tech company that is actually profitable and growing fast.

Analysts estimate these side businesses provide a safety net of $5-$8 per share in value, regardless of what happens with the cloud.

Verdict

Nebius Group is a bet on the physical infrastructure of the future.

It is not a safe, steady dividend payer.

It is a company building the railroad tracks for the next industrial revolution.

The Risks:

Building these AI factories is expensive. Nebius plans to spend $5 billion in 2025 just on buying chips. They are currently losing money (~$100M net loss last quarter).

If Microsoft cancels the contract (unlikely, but possible), the stock would implode.

If you believe that we are in the early innings of a massive shift toward automated intelligence, Nebius offers one of the purest, most aggressive ways to invest in that future.

They are backed by top-tier engineering, massive contracts from the biggest companies on earth, and a “born rich” balance sheet that gives them a distinct advantage over the competition.

The next twelve months will determine whether Nebius becomes one of the two or three dominant providers alongside CoreWeave or becomes a solid but not spectacular single-customer infrastructure company.

Investors who buy today are essentially taking a bet that the pipeline of additional hyperscaler deals materializes.

If they announce a deal with Google or Amazon next? The stock won’t just walk, it will sprint.

If you made it to the end, hit like, restack it, and share it with someone who’d get value from it. Seriously, it helps more than you realize.

Disclaimer: Nothing in this newsletter is financial advice. All opinions, analyses, and commentary shared here are my own personal views, based on publicly available information and independent research. You should not rely on any of this content as a recommendation to buy, sell, or hold any security or investment. Always do your own due diligence and consult a licensed financial advisor before making investment decisions.

Thanks for this👍

Thanks for sharing another story about your investments! I enjoy reading your stories about stocks

and your in-depth analyses.