This is how recessions start

Not one shock, but three.

On Monday morning, a 67-year-old Austrian economist named Jan Hatzius updated a number on a Goldman Sachs internal model.

He changed it from 25% to 30%, marking the third time he’d adjusted that number in 90 days.

The number is Goldman’s probability of a US recession in the next twelve months.

It was 20% at the start of the year, 25% eleven days ago, and now it’s 30% today.

Hatzius isn’t dramatic, he doesn’t go on CNBC to scream about crashes.

He’s the kind of guy who lets the data do the talking and then updates his model accordingly.

Which is exactly what makes this worth paying attention to.

Most recession calls focus on one big, scary thing, a housing crash, a banking crisis, or a pandemic.

The US’s current situation is different, it’s not one catastrophic event, but three completely separate problems that all showed up at the same time.

And the terrifying part isn’t any single one of them, it’s the math when you stack them on top of each other.

The stack

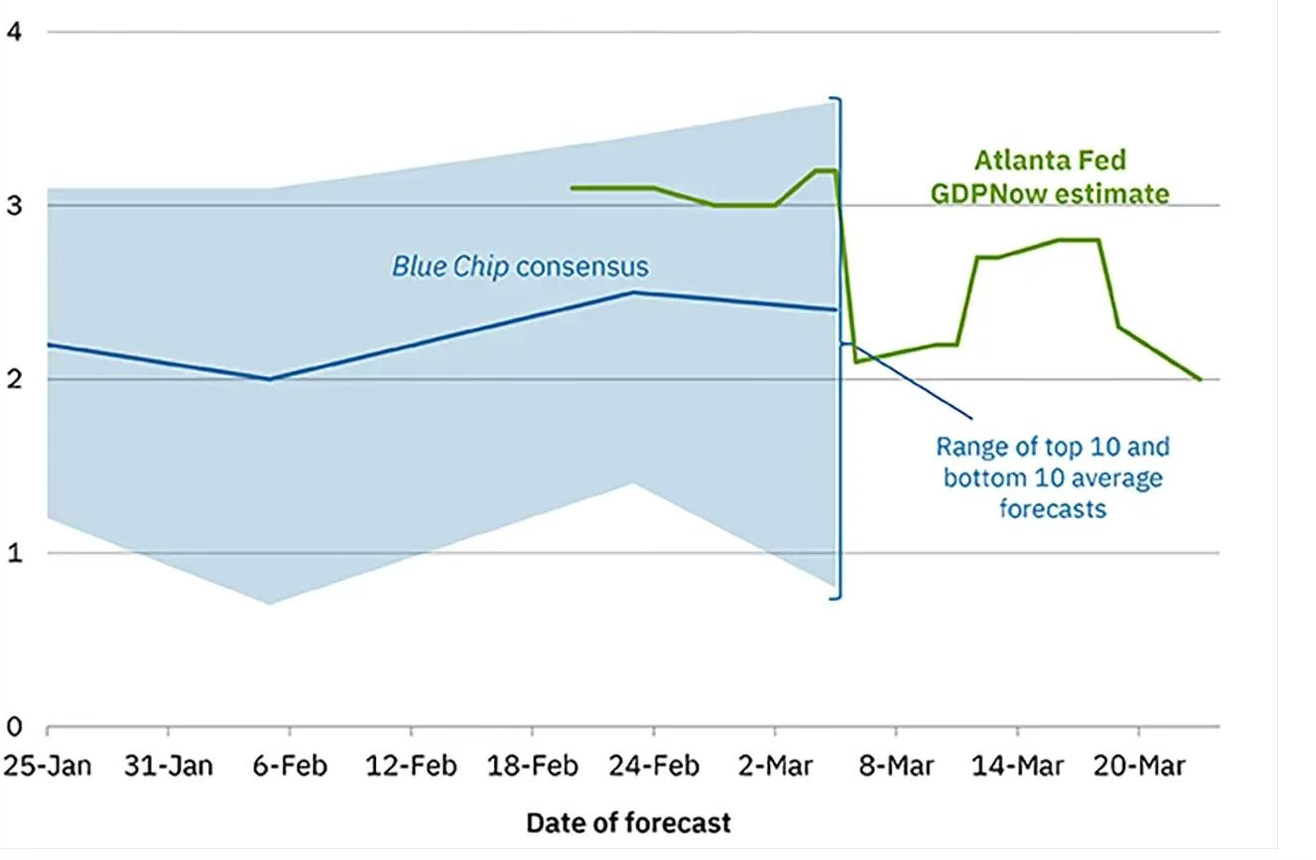

Let’s start with the fastest-moving piece. The Atlanta Fed runs a live GDP tracker called GDPNow.

It’s a real-time read that updates every time new economic data hits, think of it as the economy’s live box score.

On February 24, Q1 2026 growth was tracking at a healthy 3.1% annualized with no red flags.

Here’s what happened over the next four weeks:

• Feb 27: 3.0%. Barely moved.

• Mar 6: 2.1%. Oh.

• Mar 13: 2.7%. Small bounce from inventory data. Don’t get excited.

• Mar 19: 2.3%. Construction spending cratering.

• Mar 23: 2.0%. Private fixed investment just fell off a cliff from 3.1% growth to 1.2% in a single release. Residential investment, non-residential structures, and private inventories all dropped simultaneously.

1.1 percentage points were wiped out in under a month.

Goldman’s own estimate of US potential GDP growth, the speed at which the economy needs to grow just to keep the unemployment rate from rising, is 2.3%.

We are now below it and still falling.

Goldman’s H2 2026 forecast is 1.25%–1.75%, and for the second half of this year, the economy is expected to grow more slowly than it needs to just to tread water.

That gap between what the economy is producing and what it could be producing has a name when it gets wide enough.

It’s called a RECESSION.

Problem 1: The oil shock that broke all the records

The Strait of Hormuz is closed.

That’s the 21-mile-wide chokepoint between Iran and Oman that handles roughly 20% of the world’s entire oil supply, about 20 million barrels a day.

Every barrel flowing from Saudi Arabia, Iraq, UAE, Kuwait, and Iran to the rest of the world passes through it.

Here’s the precedent table:

• 1973 OPEC Embargo (+300% oil): 16-month recession and the stagflation era begins. Gerald Ford hands out “WIN” buttons (Whip Inflation Now). It does not work.

• 1979 Iran Revolution (+100%): Double-dip recession through 1980–82. The Fed raised rates to 20%.

• 1990 Iraq-Kuwait invasion (+135%): 8-month recession. The S&L (savings and loan) crisis piled on.

• 2008 Oil Peak at $147 (+96%): The Great Recession, eighteen months and you know how this one ended.

• 2026 Hormuz Crisis (+60% and counting): TBD.

The correlation between the magnitude of an oil price spike and the severity of the recession that follows is 0.9.

Among the highest of any leading indicators in the entire field of economics.

Every single major oil supply shock in modern history ended in recession.

Brent crude is at $110, and Goldman expects it to stay there through April.

Fitch says if the closure runs six months, we’re looking at a $120 annual average, with spikes to $130–$170 and the record is $147.50, set in July 2008.

You know what happened in Q4 2008.

Problem 2: The fiscal tailwind wore off

Remember the One Big Beautiful Bill from last summer?

The mammoth tax package that reinstated 100% bonus depreciation, doubled the Section 179 expensing cap to $2.5 million, gave full expensing for new factory construction, and cut middle-class taxes?

This was the key driver of the economy’s strong Q4 2025 and Q1 2026 performance.

The problem with front-loaded fiscal stimulus is the word front-loaded.

Businesses that rushed to claim first-year expensing in 2025 already did it, and they don’t need to do it again.

The consumer tax cuts delivered their maximum marginal impact in year one, after that, spending adjusts, and the boost fades.

The CBO itself projects real GDP growth decelerates from 2.2% in 2026 to 1.8% in 2027, partly because this boost doesn’t repeat.

The tailwind is turning into a headwind right now.

Problem 3: Money just got more expensive

When oil spikes, financial conditions tighten. Goldman’s proprietary Financial Conditions Index, a composite measure of how easy or hard it is to borrow, invest, and take risk, has tightened by roughly 60 basis points since the Hormuz crisis started.

What that looks like in the real world:

• Airlines down 14–20% (jet fuel is their biggest cost)

• Cruise lines down 20%+

• S&P 500 dropped 3% in the first few trading days

• Financial sector down 4% in March alone

This tightening alone shaves half a percentage point off H2 GDP growth.

Through tighter credit spreads, higher equity volatility, a stronger dollar squeezing exporters, and rising mortgage rates cooling housing.

And these effects compound with the typical 2–3 quarter lag, meaning the full damage from today’s tightening doesn’t show up in the data until late 2026 or early 2027.

Half a point sounds manageable but when your baseline is already 1.5% growth, half a point is not manageable.

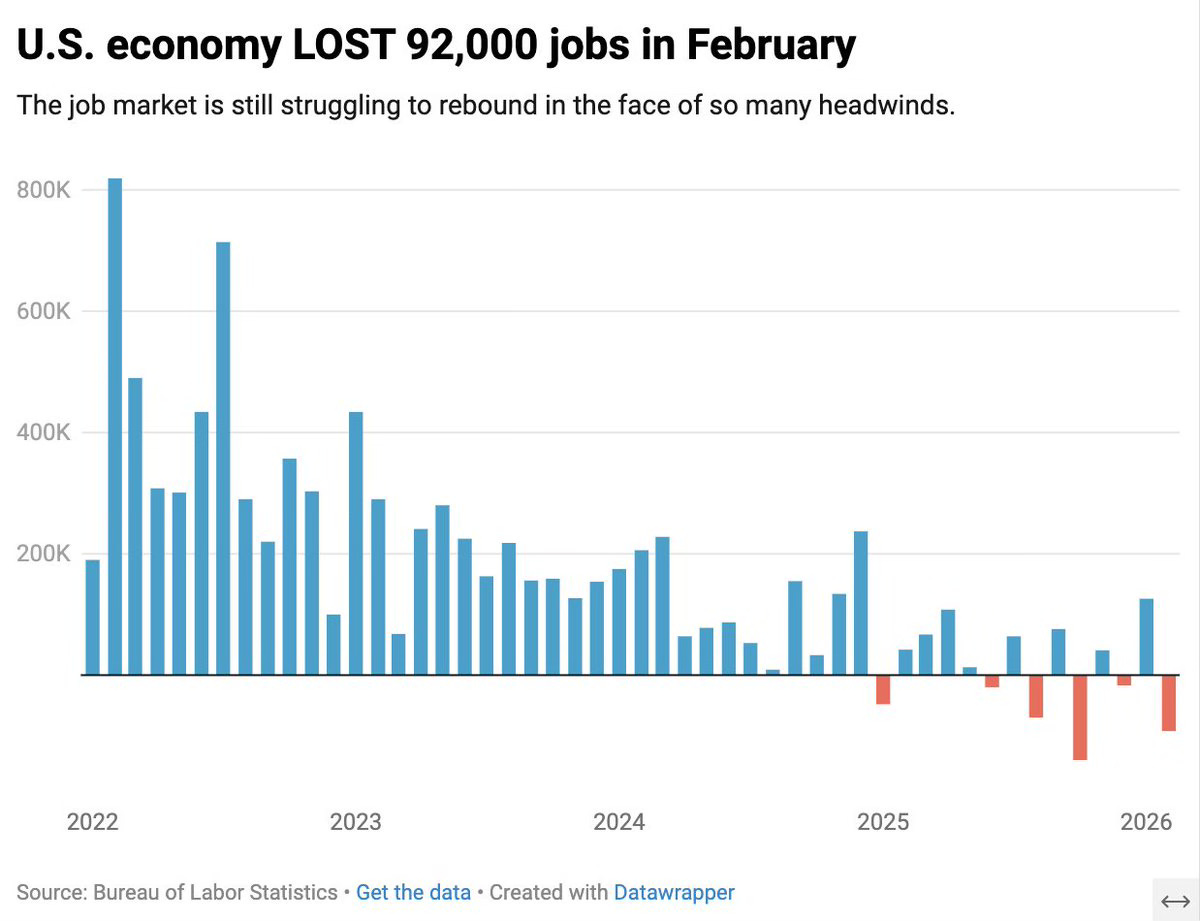

Three problems, all arriving at once in an economy that just printed –92,000 jobs in February.

The breakeven rate, or the number of jobs needed to be added monthly to keep unemployment flat, is about 70,000. The underlying trend is running at around 11,000.

The unemployment rate is already at 4.44% and is expected to rise to 4.6% by year-end, with a worst-case scenario of 4.8–4.9%.

The Sahm Rule, one of the most reliable recession indicators ever developed, triggers when unemployment rises 0.5 percentage points from its cycle low.

We are close enough to see it from here.

THE SECOND SHOE

Right now, markets are running the inflation script: oil goes up, yields go up, central banks stay hawkish, equities hold because growth is resilient.

The oil shock is being read purely as a cost-push inflation event.

The regime flip happens when the market starts pricing the other side, the demand destruction embedded in sustained $110 oil, because here’s what $110 oil actually does to an economy.

It’s a tax, a regressive, non-discretionary, unavoidable tax on every consumer and every business that uses energy, transportation, or petrochemical inputs, which is all of them.

Money spent at the pump doesn’t make it to restaurants, trucking costs push up prices and squeeze margins, airlines burn cash, and manufacturers cut shifts.

The demand destruction doesn’t show up immediately, and it shows up in the data 60, 90, 120 days later.

When it does, when the GDP prints come in, when the layoffs register in the jobs report, when the earnings revisions start rolling in, Goldman says the market’s regime assumption flips.

And when it flips:

• Oil up = yields DOWN (growth fear drowns out inflation fear)

• Oil up = stocks DOWN HARD (earnings expectations get slashed)

• The Fed pivots from holding rates to cutting rates aggressively

The 2008 playbook is clear: oil peaked at $147, the recession deepened, the Fed cut to zero, and equities fell over 50% before recovering.