Oracle Broke the AI Capital Cycle and Now Everyone’s Paying the Price

CDS is ripping, capex is exploding, and the market just realized this race isn’t funded by cash anymore.

Remember the guy from The Big Short who bet against the housing market?

The one played by Ryan Gosling who sold credit default swaps while smirking like he knew the punchline?

That was Greg Lippmann.

He worked at Deutsche Bank and Deutsche Bank is back, baby, only this time they’re looking for ways to short AI stocks while financing the entire data center boom.

According to the Financial Times, Deutsche Bank has become the biggest player in AI infrastructure lending.

They’ve pumped billions into data centers for Alphabet, Microsoft, and Amazon, just in the past two months, they helped Swedish EcoDataCenter and Canadian 5C raise over $1 billion.

Executives inside these bank are panicking. They’ve started exploring ways to short baskets of AI stocks and buy default protection as a way to protect themselves.

So, why are they doing this? Because the last thing they want is a repeat of 2008 on their balance sheet.

They remember exactly what it felt like to be holding the bag when the whole system blew up, and they’re not about to run that playbook again.

So they’re hedging the only way a bank knows how: bet on the boom, insure against the bust.

And is everyone doing that? Absolutely not.

Now here’s where this actually gets interesting.

The First Major Red Flag

In my Nov 4th edition, I said earnings were being foreshadowed and AI capex announcements weren’t moving stocks anymore.

They stopped being bullish.

And now we have the clear answer

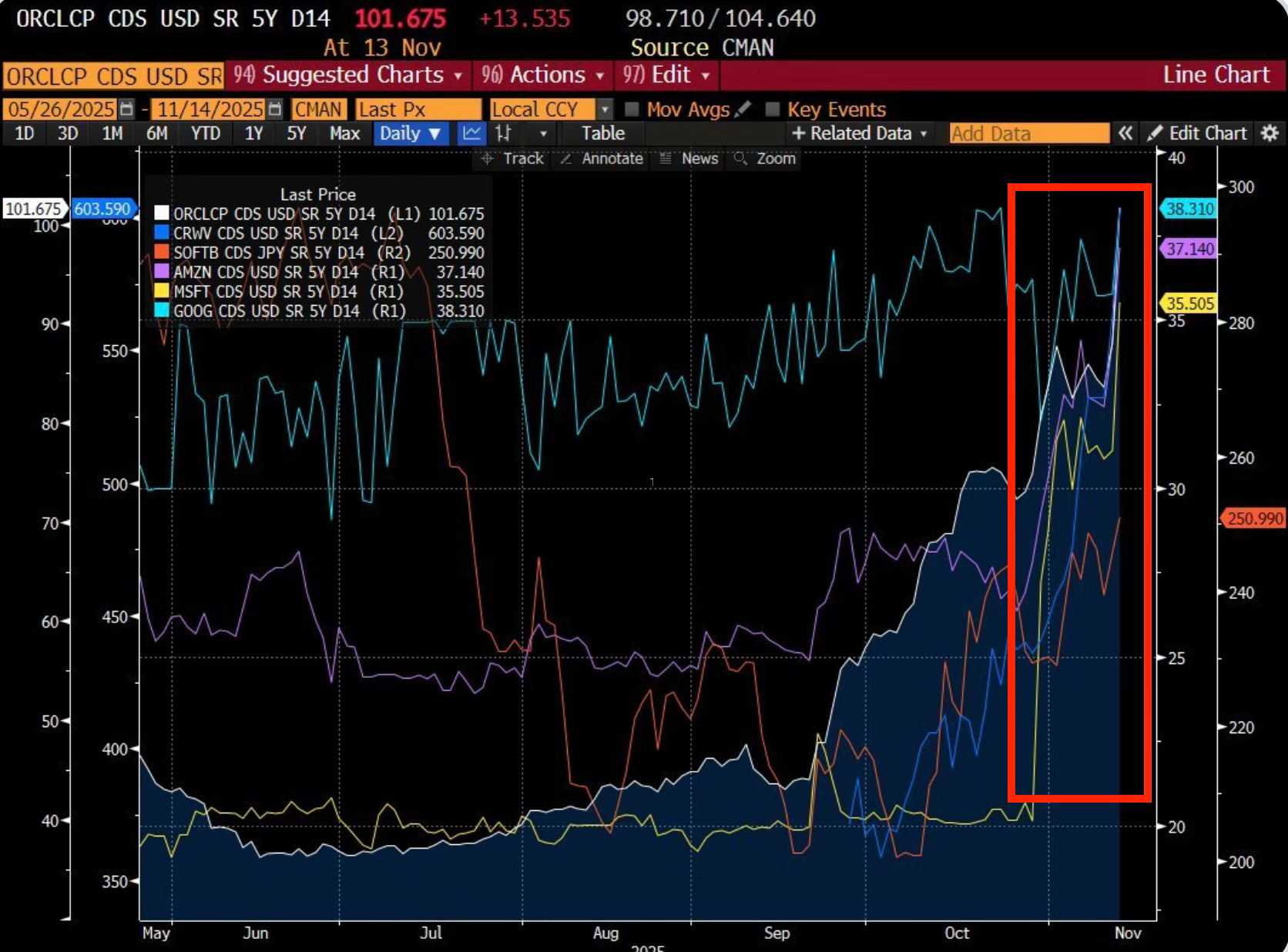

Let me present you with a chart that should honestly worry you.

You might be wondering what am I even looking at here.

You are looking at CDS, the same thing Lippmann used to bet against housing is ripping higher across literally every company tied to AI capex. Oracle, Snowflake, Amazon, Google all of them.

Credit markets don’t just casually move like this.

And it makes total sense.

These companies went from being asset light cash machines to suddenly taking on massive debt, buying hardware, loading up on GPUs, and burning cash to keep up with this AI race.

Five years ago they were swimming in free cash flow. Now they’re basically building factories and amortizing everything to death.

This is the first real sign that the market is starting to price in the downside of the AI boom.

And you should pay very close ATTENTION.

How We Got Here?

Let’s back up and see exactly how we ended up in this position.

This whole thing really snapped into focus on September 10, when Oracle dropped this massive, five-year, $300B cloud deal with OpenAI like it was nothing.

The stock ripped, everyone cheered and then people noticed the fine print.

Oracle had stacked up over $300B in “future revenue” from just a handful of customers and acted like this was all locked in.

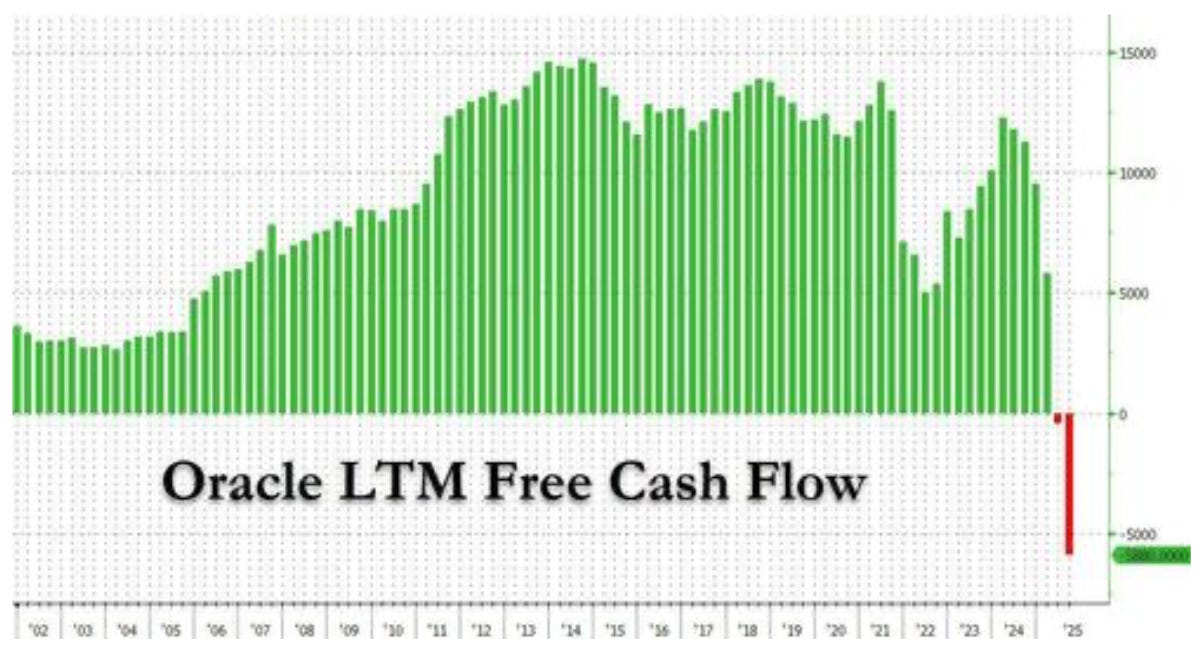

That hype only lasted about a few weeks until everyone realized Oracle didn’t actually have the cash to build any of this out.

They could have avoided some embarrassment if it hadn’t also highlighted that it doesn’t actually have the funds for this long-term spending spree projected to stretch into the 2030s.

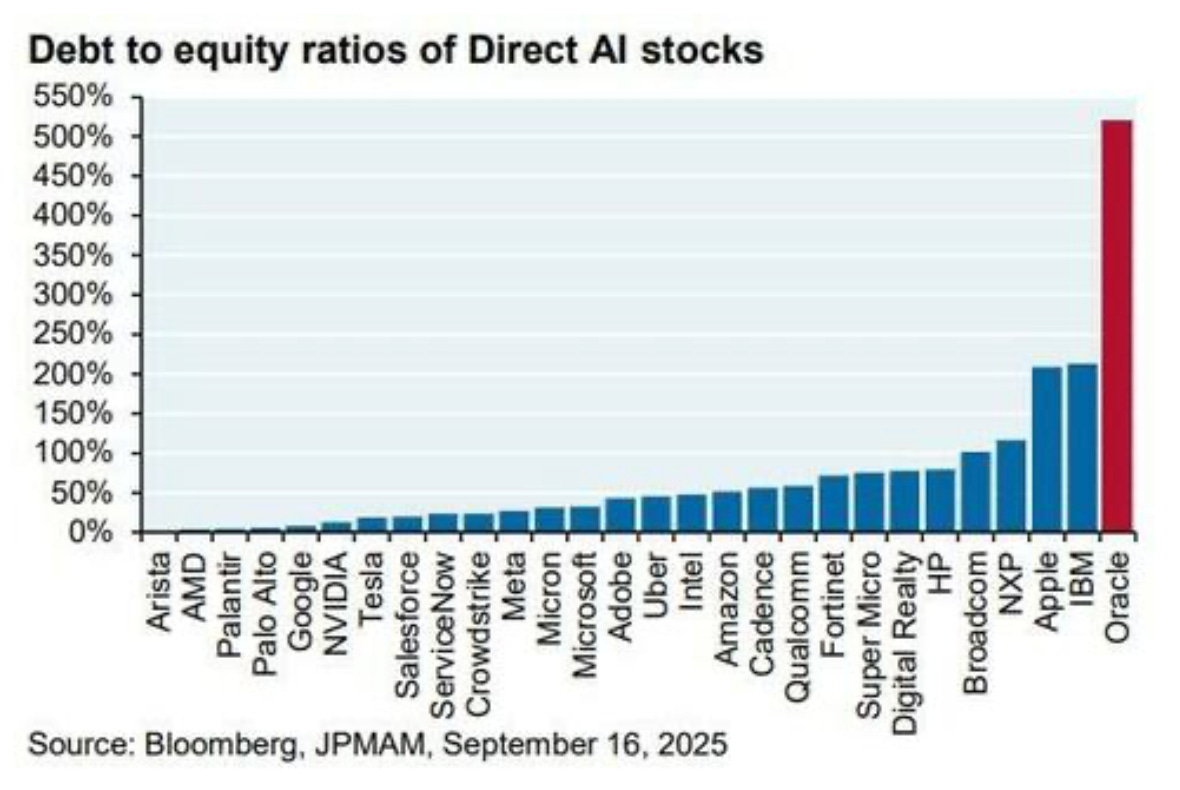

JPM’s Michael Cembalest highlighted the issue in a note:

Oracle’s stock surged by 25% after being promised $60 billion a year from OpenAI, a sum OpenAI hasn’t earned yet, to provide cloud computing facilities that Oracle hasn’t built yet, and which will require 4.5 GW of power (equivalent to 2.25 Hoover Dams or four nuclear plants), along with increased borrowing by Oracle, whose debt to equity ratio is already 500%, compared to 50% for Amazon, 30% for Microsoft, and even less for Meta and Google. In other words, the tech capital cycle may be on the brink of change.

What made this even worse is what it revealed about the entire AI infrastructure race.

Up until Oracle jumped in, the hyperscalers were funding this build-out with their own cash.

Amazon, Microsoft, Google, they were burning free cash flow to build data centers, expand power, buy GPUs, add racks, beef up networking, and cover the cooling and land and energy needs that come with it.

It wasn’t cheap, but they could handle it.

Oracle shattered that balance.

Consider Becoming a Paid subscriber to keep reading: These deep dives takes hours of work. Upgrade for just $99 a year (others charge $100+ monthly) to keep this newsletter going and get the insights that really matter.

Keep reading with a 7-day free trial

Subscribe to Investinq to keep reading this post and get 7 days of free access to the full post archives.